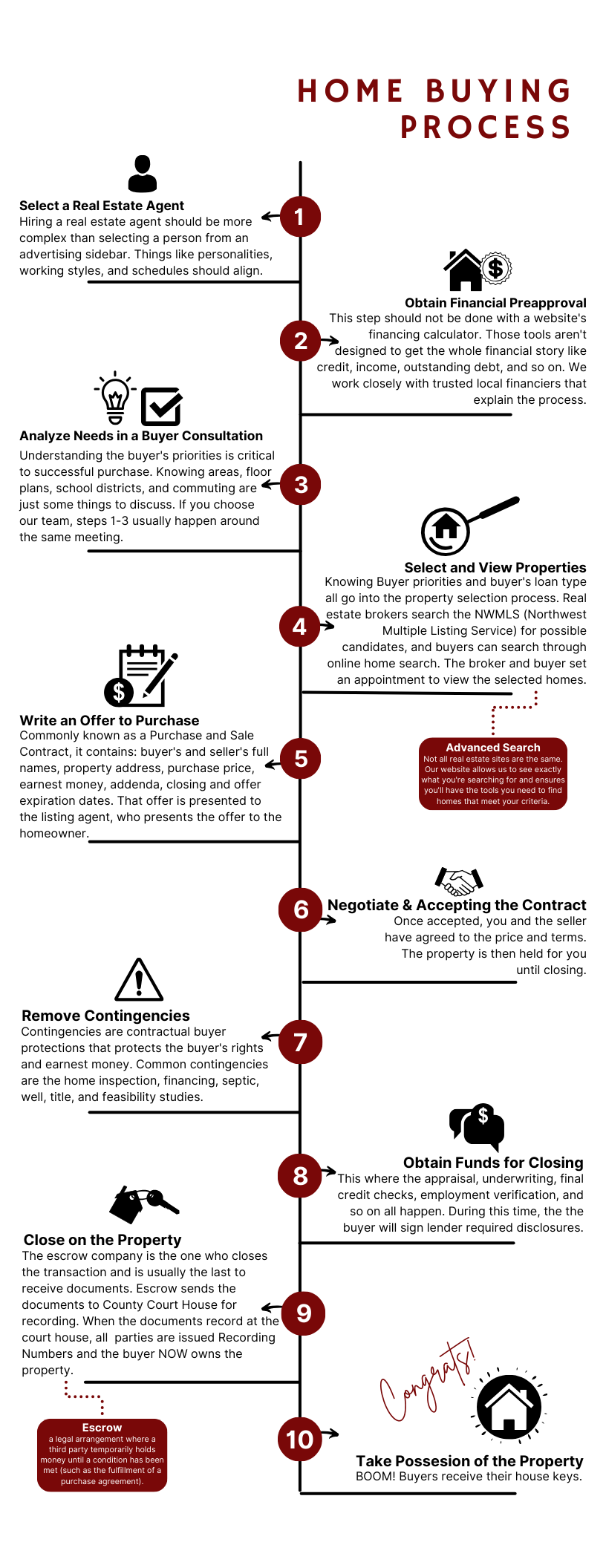

First-time home buyers often face hurdles that can make the dream of homeownership feel distant. With rising property prices, a competitive housing market, and the burden of student loans, many potential home buyers struggle to save enough for a down payment. A new initiative has emerged, offering a $7,500 government grant designed to ease financial burdens for first-time home buyers. This article explores the details of the program, eligibility requirements, and tips for navigating the home-buying process.

What is the $7,500 Government Grant for First-Time Home Buyers?

The $7,500 government grant is a financial assistance program aimed at helping first-time home buyers cover the down payment and closing costs associated with purchasing a home. The grant can significantly reduce the upfront costs of buying a house, making homeownership more accessible for those who may otherwise be delayed by financial constraints.

Understanding the Grant Program

The government grant aims to assist low to moderate-income families who are purchasing their first home. The funds can be applied towards the down payment, closing costs, or any other necessary expenses related to obtaining a mortgage.

Grant Availability and Funding

The program represents part of a broader initiative by state and federal governments to bolster homeownership rates and stimulate economic growth. The availability of the grant may vary based on state and local programs, with some areas offering additional financial incentives.

| State | Grant Amount | Program Availability | Additional Assistance Options |

|---|---|---|---|

| New York | $7,500 | Year-round | Homebuyer education programs |

| California | $7,500 | Ongoing | Low-interest loans |

| Florida | $7,500 | Annual funding limit | Closing cost assistance |

| Texas | $7,500 | Limited availability | Matching grants |

Key Features of the Grant

- Non-repayable: Unlike loans, this grant does not require repayment, provided that the buyer meets the program’s requirements.

- Flexible Use: Buyers can use the funds for various expenses beyond just the down payment, such as closing costs, inspection fees, and homeowner insurance.

- Direct Payments: The grant is typically disbursed directly to the lender or closing agent at the time of closing, streamlining the process for buyers.

Eligibility Requirements

To qualify for the $7,500 grant, applicants must meet specific criteria. Generally, the requirements include:

Financial Criteria

- Income Limits: Applicants must have a household income below 80% of the area median income (AMI). This figure can vary significantly based on location.

- Credit Score: While some programs may have flexible credit requirements, a score of at least 620 is often recommended for conventional loan eligibility.

Homebuyer Status

- First-Time Homebuyer: The definition of a first-time homebuyer may include anyone who has not owned a home in the past three years.

- Primary Residence: The home must be used as the buyer’s primary residence. Buyers looking for investment properties will not qualify.

Additional Requirements

- Homebuyer Education Program: Many states mandate that participants complete a homebuyer education course to ensure they understand the responsibilities of homeownership.

How to Apply for the Grant

- Research Local Programs: Begin by visiting your state or local housing authority website to find specific programs that may offer the grant or similar assistance.

- Gather Documentation: Prepare necessary documents, including financial statements, credit reports, and proof of income.

- Complete Application Forms: Fill out the grant application, ensuring that all information is accurate to avoid delays.

- Attend Homebuyer Education Classes: Complete any required educational segments to fulfill program requirements.

- Submit Applications: Send your completed application and supporting documents to the relevant housing authority or lender.

Pros and Cons of the Grant

Pros

- Reduced Financial Burden: The grant significantly lowers upfront costs, making homeownership attainable for many.

- Non-Repayable: The grant does not require repayment, unlike loans, reducing long-term financial stress.

- Accessible Options: The grant is available in multiple states and often combines with other assistance programs for additional support.

Cons

- Income Limits: The program primarily targets low to moderate-income buyers, excluding higher-income families.

- Program Variability: Availability and specific terms of the grant can differ widely depending on location and funding levels.

- Application Process: The application process can be time-consuming, with some paperwork and documentation requirements.

Alternatives to the $7,500 Grant

For those not qualifying for the $7,500 grant, several alternatives exist:

FHA Loans

Federal Housing Administration (FHA) loans allow for lower down payments (as low as 3.5%) and are accessible to buyers with lower credit scores.

USDA Loans

These loans are specifically designed for rural and suburban homebuyers and can offer 100% financing, eliminating the need for a down payment.

State and Local Grants

Many states and municipalities offer their own homebuyer assistance programs. Researching local options may yield additional resources to help with the home buying process.

| Alternative Program | Eligibility Criteria | Benefits |

|---|---|---|

| FHA Loans | Lower credit score | Low down payment |

| USDA Loans | Rural area residency | 100% financing |

| Local Grants | Varies by region | Up to $10,000 assistance |

Final Thoughts

The $7,500 government grant offers a significant opportunity for first-time home buyers to enter the housing market. By understanding the eligibility requirements, application process, and available alternatives, potential homeowners can better navigate the complexities of purchasing their first home. With careful planning and the right resources, achieving homeownership can transform from a distant dream into a tangible reality.

{kind=link}